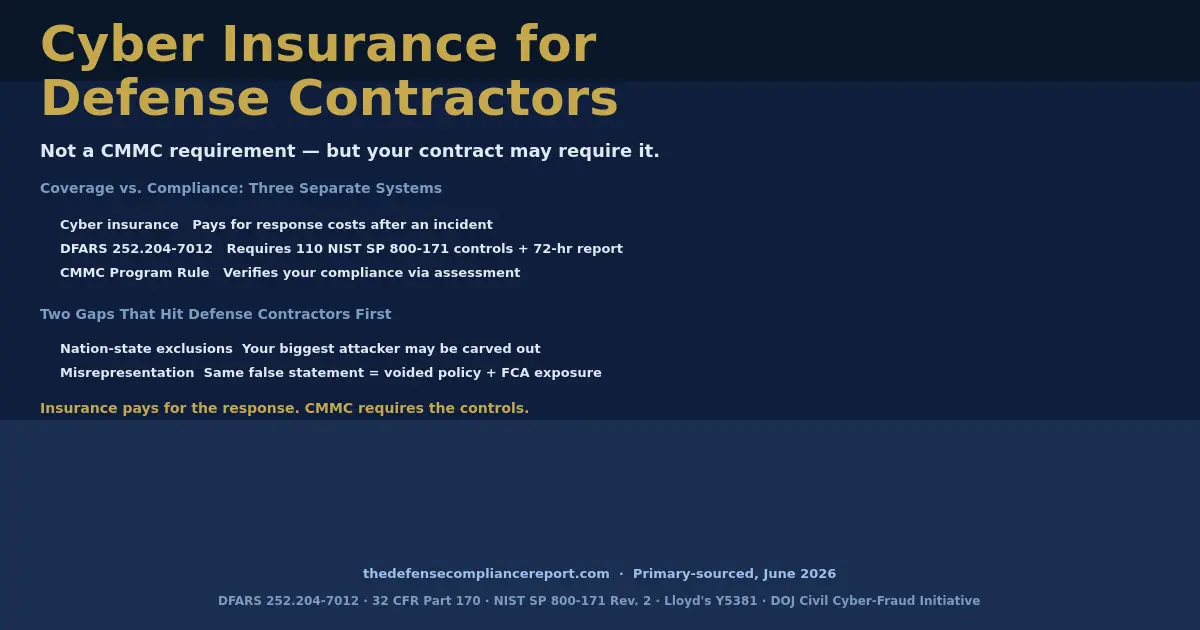

Cyber Insurance for Defense Contractors

Cyber insurance for defense contractors is not, by itself, required by any government-wide FAR or DFARS clause — but it is often required by your contract. What is mandatory, if your DoD contract contains DFARS 252.204-7012, is providing adequate security through NIST SP 800-171 and reporting cyber incidents to the Department of Defense within 72 hours. Buying cyber insurance does nothing for your CMMC status. These are separate jobs.

The rest of this page is the part nobody else assembles: where insurance and your defense obligations don’t line up, the two coverage gaps that hit defense contractors specifically, and the one move that quietly improves both your insurability and your contract eligibility at the same time.

Which system does what — read this first

Most of the confusion on this topic comes from treating cyber insurance, CMMC, and DFARS as one thing. They’re three. Here’s the clean separation.

| System | What it actually does | What it does not do | Primary authority |

|---|---|---|---|

| Cyber insurance | Helps pay for covered losses after an incident: breach response, forensics, data restoration, business interruption, legal defense, some third-party claims | Prove CMMC compliance; guarantee payment for every cyber event; discharge your duty to report to DoD | Policy wording (carrier-specific) |

| DFARS 252.204-7012 | Requires “adequate security” via NIST SP 800-171 and rapid cyber-incident reporting to DoD when the clause is in your contract | Sell insurance or set a coverage limit | Acquisition.gov, DFARS 252.204-7012 |

| DFARS 252.204-7025 (solicitation provision) | Puts you on notice, before award, of the CMMC level the contract requires; you need current status in SPRS to be eligible | Carry the ongoing obligation (that’s 7021’s job) | Acquisition.gov, DFARS 252.204-7025 |

| DFARS 252.204-7021 (contract clause) | Requires you to maintain the contract-specified CMMC status during performance, post results in SPRS, and affirm compliance annually | Replace your policy, its exclusions, or a broker’s coverage review | Acquisition.gov, DFARS 252.204-7021 |

| NIST SP 800-171 Rev. 2 | Defines the 110 requirements across 14 families used for CMMC Level 2 | Tell you what insurance limit to buy | NIST CSRC, SP 800-171 Rev. 2 |

| Licensed cyber broker / counsel | Interprets policy wording, limits, exclusions, endorsements, claims duties | Implement CMMC controls or certify your CMMC status | Professional role |

Map your situation to the right CMMC provider category

The right CMMC provider isn’t the same for every contractor — the category you need (a C3PAO, an RPO, an MSSP, a GRC platform, or a CUI enclave) depends on your required CMMC level, whether you handle FCI or CUI, your assessment type, your cloud and IT environment, and your contract timeline. The contract clause sets your level, not a checklist.

Is cyber insurance required for defense contractors?

No single FAR or DFARS clause requires a defense contractor to buy cyber insurance. What’s mandatory under DFARS 252.204-7012 — when that clause is in your contract — is providing adequate security through NIST SP 800-171 and reporting cyber incidents to DoD within 72 hours. You may still be contractually required to carry cyber liability coverage by your prime’s flow-down terms, a specific solicitation, a lender, or a customer. So “required” depends on your contract, not on a regulation.

This trips people up constantly, so let’s be precise. There are two different obligations, and they get tangled.

The federal cybersecurity obligation is real and it is not optional. DFARS 252.204-7012requires adequate security on covered contractor information systems by implementing NIST SP 800-171. In May 2024, DoD issued a class deviation directing contractors subject to DFARS 252.204-7012 to keep complying with Revision 2 — so Rev. 2’s 110 requirements remain the operative standard, not the newly published Rev. 3.

CMMC certification is also phasing into contracts now: Phase 1 began November 10, 2025 (primarily Level 1 and Level 2 self-assessments) and Phase 2 begins November 10, 2026(adding Level 2 C3PAO certification). For a growing share of awards, the assessment piece is moving from “someday” to “this solicitation” — which is usually the moment a contractor starts getting prime questionnaires and insurance applications at the same time, and starts confusing the two.

The insurance obligation, when it exists, comes from somewhere else entirely — your contract, not the regulation. Subcontractors most often meet cyber insurance as a flow-down requirement: a prime’s subcontract specifies a minimum limit, an additional-insured endorsement, or “primary and non-contributory” wording.

So the practical answer to “do I need it” is: read the actual agreement in front of you. Find the insurance clause in the subcontract or solicitation, note the required limit and coverage type, and confirm the certificate language and any additional-insured requirement. Then — separately — confirm whether the same document is also asking for CMMC status, an SPRS score, NIST 800-171 evidence, or proof of how you handle CUI. Those are different asks that often arrive in the same email.

And the most expensive misunderstanding in this entire topic, said plainly: buying cyber insurance does nothing for your CMMC status. It is not a control. It does not get logged in the Supplier Performance Risk System (SPRS). It will not satisfy a self-assessment or a C3PAO certification assessment. Treat it as financial risk transfer, full stop.

Not sure whether your issue is insurance, CMMC, or contract scope? Find My CMMC Path will sort it — give us your level, FCI/CUI scope, and timeline and we’ll route you to the provider category that fits. No CUI, drawings, or sensitive contract details, please.

A quick note on NIST 800-171 Rev. 2 vs. Rev. 3

NIST published SP 800-171 Revision 3 on May 14, 2024, and marks Revision 2 as superseded. For defense contracts, though, Revision 2 is still the operative standard. In May 2024 DoD issued a class deviation directing contractors subject to DFARS 252.204-7012 to keep complying with Revision 2, and the CMMC Program Rule (32 CFR Part 170) incorporates Revision 2 for Level 2.

If you’re a CISO who saw “Rev. 3” and started to panic that your whole program is outdated, breathe. Rev. 3 reorganized the controls and trimmed the count from 110 to 97, and DoD has signaled it will eventually move there — but it hasn’t yet, and it won’t until it amends the rule and prepares its assessors. Don’t let a vendor tell you Rev. 3 is the CMMC standard today. It isn’t.For now, the work is Rev. 2’s 110 requirements across 14 families — and that’s what underwriters and assessors will be checking.

What does cyber insurance for defense contractors actually cover?

A typical cyber policy covers first-party costs — incident response, forensics, data restoration, business interruption, cyber extortion — and third-party liability for claims and legal defense after a breach. The operative word is “covered.” Ransomware, social engineering, war and nation-state activity, the value of stolen intellectual property, and anything tied to misrepresenting your security posture can be limited, sublimited, or excluded depending on the exact policy wording.

Cyber coverage generally splits into two halves, and you want both.

First-party coverage pays for your costs when an incident hits you directly: incident response and digital forensics (often a “breach coach” and an approved vendor panel); restoration of damaged or destroyed data and systems; business interruption and extra expense while you recover; cyber extortion and ransomware response, where covered and often sublimited; and crisis communications and customer notification.

Third-party coverage pays when someone else — a customer, a prime, a vendor, a regulator — comes after you following a breach: privacy and network-security liability; legal defense costs; and regulatory defense, where the policy includes it.

The EPA’s published cyber insurance guidance — a useful, vendor-neutral government primer — flags a truth most broker pages skip: some cyber risks are excluded unless explicitly added back, and ransomware in particular may require its own coverage grant.

Questions to ask your broker before you bind — specific to defense contractors

For a defense contractor, the questions below deserve special attention before you sign anything, because they’re where the policy and your real-world DIB risk diverge. We added an “evidence to bring” column, because the same documents that answer a broker’s question are the documents an assessor wants.

| Ask your broker, in writing | Why it matters for defense contractors | Evidence to have ready |

|---|---|---|

| Does this policy cover incidents involving CUI or covered defense information? | A CUI exposure triggers contract, prime, investigation, and 72-hour reporting consequences a generic policy may never contemplate | Your CUI data map and contract clauses |

| Is ransomware covered, sublimited, or conditioned on specific controls? | Ransomware grants are frequently capped well below the headline limit and conditioned on MFA, EDR, and tested backups | Backup architecture and a dated restore test |

| Is social engineering / funds transfer fraud included or a separate add-on? | In Coalition’s 2024 claims data, business email compromise and funds-transfer fraud were the largest share of reported claims | Email security and DMARC configuration; payment-controls procedure |

| Does business interruption extend to cloud and vendor outages? | Many DIB suppliers run on Microsoft 365, GCC/GCC High, AWS GovCloud, or a managed IT stack — the worst outage may start at a vendor | Cloud/vendor inventory and dependencies |

| How broad is the war / state-backed cyber-operation exclusion? | Defense contractors are the intended target of nation-state actors; this exclusion is not theoretical for you | The policy’s exclusion wording (read it before you bind) |

Take these questions straight to your broker before you bind coverage. And if answering them surfaced control gaps you can’t evidence yet, that’s a readiness problem, not an insurance problem — see which provider category fits.

Where cyber insurance and your DFARS/CMMC obligations don’t line up

Cyber insurance and DFARS/CMMC are two different jobs that only partly overlap. Insurance pays for the response to an incident; DFARS 252.204-7012 and CMMC require the controls that prevent it and the reporting that follows. A policy never discharges your 72-hour reporting duty, never makes you compliant, and — critically — generally will not cover False Claims Act exposure arising from misrepresenting your compliance.

We built the table below because no broker page and no CMMC vendor page puts these two columns side by side. It’s our Obligation Gap Map: for each exposure a defense contractor actually carries, what the regulation requires, what a typical policy covers, and the gap that’s left in the middle. Read it as a checklist of conversations to have before you renew.

| Your exposure | What DFARS/CMMC requires | What a typical cyber policy covers | The gap to close | Authority |

|---|---|---|---|---|

| CUI / covered defense information breach | Adequate security via NIST SP 800-171 Rev. 2 (110 requirements) | First-party breach response, forensics, notification, restoration; third-party liability | The policy pays for response; it does not make you compliant or excuse a controls failure | DFARS 252.204-7012(b); NIST SP 800-171 Rev. 2 |

| 72-hour DoD incident reporting | Report to DoD via DIBNet within 72 hours; preserve images 90 days; submit malware to DC3 | IR vendor and breach-coach costs are often covered | Coverage helps with the cost of response — not the legal duty to report on time. That duty is yours | DFARS 252.204-7012(c)–(g) |

| Nation-state / advanced persistent threat (APT) attack | Implement controls; CMMC Level 3 adds NIST SP 800-172 requirements aimed at advanced threats | Often narrowed or excluded by war / state-backed / “cyber-operation” exclusions adopted since 2023 | The exact adversary that targets defense work is the one your policy may carve out. Read the state-backed clause word for word | Lloyd’s Bulletin Y5381 (eff. Mar. 31, 2023); Merck v. ACE American |

| Misrepresenting your security posture (on an insurance application or a DoD affirmation) | A true, current CMMC affirmation and an accurate SPRS score | Excluded — fraud / intentional-acts / known-falsity provisions; the policy can be rescinded for application misstatements | One false “yes” on MFA or controls can void your policy and expose you to the False Claims Act. Same act, two catastrophes | Insurer rescission actions; DOJ Civil Cyber-Fraud Initiative |

| False Claims Act / DOJ cyber-fraud liability | Don’t knowingly submit false cyber-compliance claims; correct inaccurate ones | Cyber policies generally do not cover FCA treble damages or penalties | This is the uninsured tail. DOJ frames these cases as built on misrepresentations, not breaches | Georgia Tech $875K; MORSE $4.6M; Raytheon $8.4M |

| Subcontractor / supply-chain flow-down | DFARS 252.204-7012 flows down for operationally critical support; CMMC flows down where subs process, store, or transmit FCI/CUI | Your policy covers you; contingent / third-party business interruption varies | A sub’s breach can hit your contract and reputation — confirm your contingent and third-party limits | DFARS 252.204-7012(m); 32 CFR Part 170 |

| Prime-imposed insurance requirement | Not a DFARS mandate — a contract term | The policy you buy to satisfy it | Match the limit, additional-insured, and “primary/non-contributory” wording to the flow-down exactly | Your subcontract (verify your clause) |

The takeaway, stated cleanly so you can quote it to your CFO: cyber insurance pays for the response to an incident; DFARS and CMMC require the controls that prevent it and the reporting that follows. A policy does not make you compliant, and compliance does not replace a policy. The two most dangerous gaps for defense contractors are nation-state exclusions and misrepresentation — because the second one can void your coverage and trigger the False Claims Act at the same time.

The fix for all of this is the same

A true NIST SP 800-171 posture makes your insurance application, your SPRS score, and your DoD affirmation all defensible at once. Use Find My CMMC Path to get matched with the readiness provider category — an RPO, an MSSP, a GRC platform, or a CUI enclave — that builds and documents it. Do not submit CUI, drawings, or sensitive contract details.

Route to the right provider category →When cyber insurance won’t pay: war exclusions, misrepresentation, and the False Claims Act trap

Three things most often stop a defense contractor’s cyber claim or create exposure no policy will cover: a state-backed or “war” exclusion — aimed at the exact threat that targets the defense industrial base; a misrepresentation on the application that lets the insurer rescind the policy; and the False Claims Act, which the Department of Justice uses against contractors who knowingly misstate cyber compliance. The trap is that a single act — claiming controls you don’t actually have — can void your coverage and trigger the False Claims Act simultaneously.

Gap one: the nation-state exclusion aimed straight at you

Defense contractors are disproportionately targeted by nation-state actors. Then read your war exclusion, because the insurance industry spent the last few years rewriting it specifically to limit that risk.

The turning point was the 2017 NotPetya attack — Russian-linked malware that tore through tens of thousands of machines worldwide. Pharmaceutical company Merck claimed roughly $1.4 billion in losses and its insurers refused, citing a “hostile/warlike action” exclusion. A New Jersey trial court (2022) and a state appellate court (May 2023) both held the war exclusion did not apply to NotPetya — until the parties reached a confidential settlement on January 5, 2024, days before oral argument, with about $700 million still in dispute (Merck & Co. v. ACE American Insurance Co.).

Two things matter for you. First, the policy that won for Merck was an all-risks property policy with old, generic war language — not a modern standalone cyber policy. Second, the industry’s response was swift: Lloyd’s of London Bulletin Y5381, effective March 31, 2023, required all standalone cyber-attack policies written at Lloyd’s (risk codes CY and CZ) to include a suitable state-backed cyberattack exclusion. The war language youface today is purpose-built to exclude state-backed operations, and it comes in variants — some require a government attribution before the exclusion bites, some don’t. Have your broker walk you through it line by line, and ask specifically whether there’s a carve-back for an organization that was an unintended bystander to a state operation.

Gap two: the lie that costs you twice

Underwriters no longer take your word for it. Applications now ask pointed, yes-or-no questions about MFA, EDR, backups, and incident response — and if a forensic review after a claim finds you didn’t actually have what you attested to, the insurer can rescind the policy as if it never existed. In a widely cited 2022 case, Travelers v. International Control Services, the insurer sued to rescind a cyber policy over alleged misrepresentations about multi-factor authentication. Treat that as the rescission risk — not a rule that every partial-MFA error automatically voids coverage, but a clear signal that an audit-backed application protects your claim.

Now hold that next to the Department of Justice. Under its Civil Cyber-Fraud Initiative (launched October 2021), DOJ uses the False Claims Act — with treble damages and whistleblower (qui tam) suits — against contractors who knowingly misrepresent their cybersecurity. In early 2026, DOJ Civil Division leadership characterized these cases as built on misrepresentations, not data breaches. You don’t need to have been hacked. You need to have said something false about your compliance.

Two settlements make the point, and we read the DOJ announcements directly:

- Georgia Tech Research Corporation — $875,000 (DOJ, September 30, 2025). DOJ alleged the affiliated lab had no System Security Plan until at least February 2020, ran without antivirus/anti-malware on covered systems until December 2021, and in December 2020 submitted a summary-level score of 98 that was premised on a “fictitious” or “virtual” environment— a score that didn’t apply to any actual system processing covered defense information. Two former members of the cybersecurity team brought the case as whistleblowers. DOJ stated the settlement resolved allegations only, with no determination of liability.

- MORSECORP Inc. — $4.6 million (DOJ, March 26, 2025).Widely described as the first FCA settlement centered on a contractor’s failure to update its SPRS score after a third-party assessment produced a lower number. DOJ’s allegations included using a third-party email host that didn’t meet FedRAMP Moderate-equivalent requirements and lacking a consolidated written System Security Plan.

Add Raytheon ($8.4 million in 2025), Aero Turbine and its private-equity owner Gallant Capital Partners ($1.75 million, July 2025), and Health Net Federal Services and Centene Corporation (over $11 million, February 2025), and the pattern is unmistakable. DOJ reported that overall False Claims Act recoveries exceeded $6.8 billion in fiscal year 2025, and cybersecurity cases have become a fast-growing share.

The synthesis no broker and no CMMC vendor will hand you:the same false statement does double damage. Say “yes, MFA everywhere” when it isn’t true, and that single misrepresentation can (1) let your insurer rescind the policy you paid for and (2) become the basis of a False Claims Act case the policy won’t cover anyway. The cheapest insurance against both is not a bigger limit. It’s a true, current security posture and honest affirmations.

Representation Risk Matrix — every place you make a cyber claim about yourself

| Where you make the claim | Who relies on it | What a false statement risks | What should exist before you sign |

|---|---|---|---|

| Cyber insurance application | The carrier | Policy rescission; denied claim | MFA/EDR/backup evidence matching every “yes” |

| Prime supplier questionnaire | Your prime | Lost subcontract; flow-down breach | A current, honest control summary you can back up |

| SPRS score | DoD / contracting officers | False Claims Act exposure (see Georgia Tech, MORSE) | A score tied to your real system, not a virtual one |

| CMMC affirmation | DoD; the affirming official personally | FCA exposure; ineligibility | Confirmed implementation, not “planned” |

| System Security Plan / POA&M | Assessors, DoD, primes | Failed assessment; misrepresentation findings | A current description of the environment as it actually is |

| 72-hour incident report | DoD (DIBNet) | Contract exposure separate from insurance | A tested incident-response plan and preserved evidence |

How CMMC and NIST SP 800-171 readiness change your cyber insurance

The controls cyber underwriters demand in 2025–2026 — MFA, EDR, tested backups, a written and tested incident response plan, patching, training, and logging — are largely the same controls NIST SP 800-171 Rev. 2 already requires of defense contractors. That means CMMC readiness and cyber-insurance readiness are mostly one project: the same evidence package can serve both an underwriter and your DFARS 252.204-7012 work.

When we lined up the standard underwriting questionnaire against NIST SP 800-171 Rev. 2, the overlap was striking. Below is our Underwriting-to-NIST SP 800-171 Rev. 2 Crosswalk: each underwriter ask, the specific 800-171 Rev. 2 requirement it supports, the evidence that serves both purposes, and the provider category that typically closes the gap.

| Underwriters ask about | Supports NIST SP 800-171 Rev. 2 | Evidence that serves both | If it’s weak, the category to consider | Common mistake |

|---|---|---|---|---|

| MFA on email, VPN, remote, admin, cloud | 3.5.3 (multifactor for privileged + network access) | Conditional-access exports, identity-provider screenshots, privileged-account list, exceptions | MSP/MSSP, RPO/RP, GRC platform | Answering “we have MFA” when it’s only on email, not admin and remote access |

| EDR / MDR on all endpoints | 3.14.2, 3.14.4, 3.14.6–7 (malicious-code protection, monitoring) | Endpoint inventory, agent-coverage report, alert workflow, response SOP | MSSP/MDR, MSP | Submitting legacy antivirus as EDR; leaving servers or laptops uncovered |

| Tested, immutable/offline backups | Underwriter / ransomware-resilience expectation. 3.8.9 covers the confidentiality of backup CUI — not restore testing or immutability | Backup architecture, dated restore-test results, immutability/segmentation evidence | MSP/MSSP, CUI enclave | Having backups that were never restore-tested — or reachable by the same compromised admin account |

| Written + tested incident response plan | 3.6.1, 3.6.2, 3.6.3 (IR capability, tracking/reporting, testing) | IR plan, tabletop record, contact tree, carrier hotline, DIBNet workflow | vCISO, RPO/RP, MSSP, IR counsel | Calling the insurer but missing the DFARS evidence-preservation and 72-hour reporting steps |

| Vulnerability / patch management | 3.11.2, 3.11.3, 3.14.1 (scan, remediate, fix flaws timely) | Scan reports, remediation SLAs, patch reports, exception register | MSP/MSSP, GRC platform | Producing a scan with no proof of closure, ownership, or exceptions |

| Security awareness training | 3.2.1, 3.2.2, 3.2.3 (Awareness & Training) | Training records, phishing-simulation results, onboarding procedure | MSP/MSSP, GRC platform | Assuming the policy automatically covers social engineering and funds-transfer fraud |

| Logging / continuous monitoring | 3.3.1, 3.3.5, 3.3.6 (audit logging, review, analysis) | Centralized log configuration, review cadence, SIEM coverage | MSSP, GRC platform | No central logs, so you can’t reconstruct what happened — for the insurer or DoD |

| Privileged access / least privilege | 3.1.5, 3.1.6, 3.1.7 (least privilege, privileged functions) | Admin-group exports, password-vault logs, just-in-time elevation records | MSP/MSSP, RPO/RP | Standing local-admin rights everywhere, which raises both premium and claim severity |

| Email security / DMARC | Supports 3.13.x (system/comms protection) and 3.14.x | DMARC enforcement reports, filtering configuration | MSP/MSSP | Treating it as optional — underwriters increasingly ask, even though it isn’t a named 800-171 control |

Read it this way:the work you do to pass a cyber-insurance underwriting review and the work you do to satisfy DFARS 252.204-7012 and CMMC are largely the same project. Build one evidence package — MFA exports, EDR coverage reports, a tested IR plan, dated restore tests, training records, your SSP and POA&M — and it serves both.

Now the place to be careful: backups. Underwriters expect immutable or offline backups with a tested restore. NIST SP 800-171 Rev. 2 is thinner here — requirement 3.8.9 covers the confidentiality of backup CUI, but it does not, on its face, require restore testing the way an underwriter (and basic ransomware survival) demands. So this is one of the few spots where doing the insurance-grade thing means going beyondthe letter of the control. Do it anyway. It’s the difference between a bad week and a closed business.

A fair question we get a lot: will CMMC certification lower my premium?Honestly — we’ve found no carrier publishing a guaranteed “CMMC discount,” so don’t bank on a number. But the logic holds: because the controls overlap so heavily, the same readiness work that earns your contract eligibility is the work underwriters reward with better terms and fewer denied claims. Marsh has reported that companies investing in controls are viewed favorably at renewal. The dual lever is real even if the discount isn’t a fixed figure.

See what building that posture actually involves

Compare the readiness categories (RPO vs. MSP/MSSP vs. GRC platform vs. CUI enclave) and get matched to the one that fits your level, scope, and timeline. For the side-by-side, our CMMC provider categories page breaks down who does what.

Match me to a readiness category →How much does cyber insurance cost for defense contractors?

There’s no fixed price. General U.S. small-business cyber premiums commonly run from about $1,000 to $7,500 a year for $1 million in coverage, driven by revenue, sector, your security controls, the limits and sublimits you choose, and your retention. Reliable defense-specific premium data is thin, so treat any single number with caution and get real quotes — but know that the same controls that lower your premium are CMMC investments you’d make anyway.

After the brutal hard market of 2021–2022 — when ransomware drove premiums up 50% to 100% in some segments — the pendulum swung back. The U.S. cyber insurance market recorded its first-ever decline in direct written premium, falling roughly 7% to about $9.14 billion in 2024, down from $9.84 billion in 2023, according to the NAIC’s 2025 Cybersecurity Insurance Market Report. Marsh reported U.S. cyber rates down 5% on average in Q4 2024, with conditions staying buyer-friendly into 2025. And yet claims rose nearly 40%, to almost 50,000 reported in 2024.

Two implications for you. First, as of 2026 the soft cycle may be ending — some forecasters expect renewed increases of roughly 15–20% over the next year — so locking in good terms while you can, and walking in with documented controls, matters more than usual. Second, rates are falling but claims aren’t, which is precisely why underwriters scrutinize controls so hard. Marsh McLennan reports that 99% of cyber applications now ask specifically about MFA.

- General small-business pricing: roughly $1,000–$7,500 per year for $1 million in coverage (Marsh McLennan, 2025), varying widely by revenue, controls, and documentation.

- The controls themselves (which double as CMMC spend): MFA commonly runs a few dollars per user per month and EDR a bit more per device per month — real money, but money you’d spend for CMMC readiness anyway that also moves your premium.

- What drives your price up or down: revenue and data sensitivity, the maturity of your documented controls, your chosen limit and retention, claims history, and your third-party/cloud dependencies.

Items where defense contractors get burned at claim time:

- Sublimits. A $2 million policy can carry, for example, a $250,000 ransomware sublimit. Know your real caps.

- Retroactive date. Incidents that began before this date aren’t covered, even if you discover them during the policy period.

- The war / state-backed exclusion (see above).

- Warranty and condition language that ties coverage to the controls you attested to — the rescission trap, in fine print.

How much coverage do you actually need?

There’s no universal number, and we won’t invent one. What we can give you is the honest set of inputs that drive the decision. Take this to your broker.

| Sizing input | Why it matters |

|---|---|

| Contract- or prime-required limit | May set a floor — check your subcontract or solicitation |

| Annual revenue | Affects underwriting and business-interruption exposure |

| Estimated downtime cost per day | Helps size business interruption coverage |

| CUI / PII / payment-data volume | Drives notification, privacy, and incident exposure |

| Cloud / SaaS / vendor dependencies | Helps you weigh dependent (contingent) business interruption |

| Current MFA / EDR / backup / IR posture | Affects both pricing and your real loss probability |

| Deductible / retention tolerance | Affects your financial resilience and your premium |

| Ransomware / social-engineering sublimits you can accept | The headline limit isn’t the number that pays in those events |

What cyber insurance questions should a defense contractor expect at renewal?

Expect direct, evidence-backed questions about MFA, backups, endpoint detection, vulnerability management, incident response, business continuity, security awareness training, vendor risk, cloud services, sensitive-data handling, claims history, and governance. Because applications vary by carrier, the durable move is to maintain a standing evidence folder rather than treating any one questionnaire as the standard.

Underwriting has quietly become a technical audit. Roughly three out of four carriers now run an external scan of your attack surface during underwriting. “Yes” is no longer enough; they want the export, the screenshot, the coverage report.

Build the folder once and reuse it for renewals, prime questionnaires, and your CMMC assessment. Populate it with:

- Identity / MFA — conditional-access policies, enrollment exports, privileged-account list

- Endpoint / EDR / MDR — agent-coverage report by device and OS

- Backups — architecture, immutability settings, and dated restore-test results

- Vulnerability management — scan summaries, patch reports, exception register

- Incident response — the plan plus a tabletop record from the last 12 months

- Business continuity — your BC/DR plan

- Security awareness — training completion and phishing-simulation results

- Vendors and subcontractors — inventory, access list, flow-down language

- Cloud — service inventory and FedRAMP Moderate evidence where covered defense information is involved

- Governance — your SSP and POA&M

Who should answer the application? Not your MSP alone, and not your broker guessing at technical detail. The EPA guidance recommends a team: leadership, finance/risk, IT/security, legal/contracting, and whoever owns your CMMC evidence.

What never to do: don’t let a broker invent technical answers; don’t let an MSP answer coverage questions; don’t answer “yes” because a control is planned; don’t write “NIST compliant” without an SSP and evidence behind it; and don’t upload CUI, drawings, or sensitive contract documents into any insurance or matching form.

What happens if a defense contractor has a cyber incident?

A cyber incident can put you on two parallel clocks at once: the insurance track (policy notice and carrier-approved response) and the contract track (DoD review and reporting). If DFARS 252.204-7012 applies, you must review for evidence of compromise, rapidly report covered incidents to DoD within 72 hours via DIBNet, preserve relevant system images for at least 90 days, and coordinate required reporting — while also meeting your policy’s notice and approved-vendor requirements.

The DFARS track (when 7012 applies):

- Review for evidence of compromise; identify affected systems, data, and accounts

- Rapidly report to DoD through dibnet.dod.mil within 72 hours (a DoD-approved medium-assurance certificate is required to file)

- Submit isolated malicious code to the DoD Cyber Crime Center (DC3) if required

- Preserve and protect images of affected systems and relevant monitoring data for at least 90 days

- Pass reporting obligations and report numbers down to and up from affected subcontractors

The insurance track:

- Notify the insurer exactly as the policy requires — late notice can imperil the claim

- Use carrier-approved breach counsel and forensics if the policy mandates it

- Preserve privilege where counsel directs

- Do not pay a ransom without insurer, counsel, and sanctions review — the Treasury Department’s Office of Foreign Assets Control (OFAC) has warned that facilitating ransom payments to sanctioned actors can carry sanctions liability

- Document the timeline, systems, costs, and decisions as you go

Which provider category should help with cyber insurance readiness?

A licensed cyber broker places and interprets your coverage, but a broker doesn’t build the CMMC evidence behind your answers. Most contractors need one or more separate lanes: an RPO/RP or vCISO for scope and documentation, an MSP/MSSP for technical controls, a GRC platform for evidence workflow, a CUI enclave for scope reduction, broker/counsel for policy wording, and a C3PAO only when you’re assessment-ready.

| What you need | Provider category | Why |

|---|---|---|

| Policy wording, limits, exclusions, claims terms | Licensed cyber broker / coverage counsel | Coverage is policy-specific and legal |

| CUI scope, DFARS applicability, SSP/POA&M planning | RPO / RP (Registered Provider Organization / Registered Practitioner); federal-contracts attorney where legal interpretation is needed | Scope and contract language set the path |

| MFA, EDR/MDR, backups, patching, logging, remediation | MSP / MSSP (Managed Security Service Provider) | These are operating controls, not paperwork |

| Evidence repository, SSP/POA&M workflow, control ownership | GRC platform | Maintains evidence for underwriting, CMMC, and renewal |

| Reduce the CUI system boundary | CUI enclave | Can simplify scope when designed correctly |

| Formal CMMC Level 2 certification assessment | C3PAO (Certified Third-Party Assessment Organization) | Only for assessment-ready organizations, when the contract requires it |

One rule we will not bend: keep readiness and assessment separate. Under the Cyber AB CMMC Code of Professional Conduct (v2.0), a C3PAO is prohibited from conducting a CMMC assessment for an organization it served as a consultant to prepare for any CMMC assessment within the previous three years. Don’t hire one firm expecting it to both fix your environment and certify it. And software alone never satisfies CMMC — a GRC platform organizes your evidence; it doesn’t implement your controls or pass your assessment.

If your insurance application exposed control gaps, don’t jump straight to a C3PAO

Find My CMMC Path will help you tell whether the next step is readiness support, managed security, an evidence workflow, a CUI enclave, broker/counsel review, or assessment planning. No CUI, drawings, or sensitive contract details.

Find My CMMC Path →Cyber insurance by contractor type: machine shops, manufacturers, SaaS, SBIRs, primes, and subs

Your business model changes the answer. A machine shop with CUI drawings, a SaaS company hosting defense data, a prime managing supplier flow-down, and a staff-augmentation sub accessing a prime’s system create different underwriting, scoping, and incident-response questions. The constant: the contract clause and your CUI handling set your obligations, not your size or your industry.

| Contractor type | Typical risk pattern | Evidence priority | Likely category |

|---|---|---|---|

| Small machine shop | CUI drawings, CNC/program files, M365, local file shares, outsourced IT | CUI data map, backups, MFA, endpoint protection, SSP, vendor access | RPO/RP, MSP/MSSP, CUI enclave |

| Aerospace / electronics manufacturer | Multiple sites, ERP, suppliers, CAD/CAM, export-controlled data | Segmented scope, vendor flow-down, business interruption, IR | RPO/RP, MSSP, GRC, broker/counsel |

| Software / SaaS subcontractor | Cloud-hosted data, source code, customer access, CI/CD | Cloud architecture, FedRAMP question, SSP boundary, vuln management | Cloud MSP, RPO/RP, GRC, counsel |

| SBIR / startup | Small team, low admin capacity, contract pressure | Don’t overbuild — scope correctly, use an evidence workflow | RPO/RP, vCISO, GRC, CUI enclave |

| Prime contractor | Supplier flow-down, questionnaires, downstream incidents | Vendor evidence, subcontract clauses, third-party risk | GRC, RPO/RP, vendor-risk support |

| Staff augmentation / services sub | May access government or prime systems without storing CUI locally | Confirm the system boundary and the contract language | RPO/RP, federal-contracts attorney |

If you’re a subcontractor, the most common version of “do I need cyber insurance” is a flow-down term in your subcontract — so match the limit and wording exactly. If you’re a manufacturer holding controlled technical drawings, your DFARS 7012 exposure is among the heaviest in the base. And if you’re a prime, remember that verifying your subs’ compliance is your risk, not just theirs.

How to buy or renew cyber insurance as a defense contractor (without a claim-time surprise)

Start 60–90 days before you need coverage, build your controls-evidence pack first (it doubles as CMMC evidence), and have a broker who understands DoD flow-downs read the war/state-backed exclusion, the sublimits, and the warranty language before you bind. The single biggest claim-time risk is attesting to controls you can’t prove — so make the application audit-backed.

- Build the evidence pack (mirror the crosswalk: MFA, EDR, backups + restore test, IR plan + tabletop, patching, training, logs).

- Ask your broker the hard questions — the war/state-backed clause variant, ransomware and social-engineering sublimits, the retroactive date, and whether your controls are written as policy warranties.

- Match the policy to your prime’s flow-down exactly — limit, additional-insured, primary/non-contributory.

Frequently asked questions

Is cyber insurance required by CMMC?

No. Cyber insurance is not a CMMC requirement under 32 CFR Part 170 or DFARS 252.204-7021. CMMC concerns your contract-specified cybersecurity status for in-scope systems; insurance is financial risk transfer. A prime or contract may separately require coverage.

Is cyber insurance required by DFARS 252.204-7012?

No. DFARS 252.204-7012 requires safeguarding covered defense information via NIST SP 800-171 and reporting cyber incidents to DoD within 72 hours when the clause applies. It is not an insurance-purchase clause.

Can cyber insurance replace CMMC compliance?

No. Insurance can help pay for covered losses after an incident, but it does not implement controls, build evidence, post an SPRS score, satisfy a self-assessment or C3PAO assessment, or change your contract-required CMMC level.

Does cyber insurance cover a CUI breach?

It may cover the response costs — forensics, restoration, notification, legal defense — depending on the policy’s wording, definitions, exclusions, and limits. It does not discharge your DFARS 72-hour reporting duty. Confirm with your broker whether incidents involving CUI and DFARS reporting costs are covered.

Does cyber insurance cover ransomware payments?

Sometimes, but ransomware coverage is frequently sublimited and conditioned on specific controls, and a payment can raise OFAC sanctions issues. Coordinate any ransom decision with insurer-approved counsel before acting.

Does cyber insurance cover nation-state attacks?

Often it’s narrowed or excluded. Since 2023, standalone cyber policies commonly carry state-backed cyber-operation exclusions under Lloyd’s Bulletin Y5381. Defense contractors are frequent nation-state targets, so review this clause and ask about bystander carve-backs.

Can my cyber insurance claim be denied?

Yes. Misrepresenting controls on the application, missing required controls at the time of the incident, or being unable to produce evidence are common reasons claims are reduced or go unpaid.

Does cyber insurance cover False Claims Act penalties?

Generally, no. False Claims Act exposure from knowingly misrepresenting cyber compliance is typically outside cyber-policy coverage, which is why an accurate compliance posture matters more than a larger limit.

Will a high SPRS score lower my premium?

There’s no guaranteed discount. A current, accurate SSP, POA&M, and evidence package can improve the underwriting conversation, but pricing depends on the carrier, your controls, limits, retention, claims history, and the broader market.

Should my MSP fill out the cyber insurance application?

Your MSP can supply technical evidence, but the application should be reviewed by the accountable business owner and, where appropriate, broker and counsel. Never let anyone answer “yes” to a control that’s only planned or partially deployed.

What if a prime asks for proof of cyber insurance?

Ask for the exact requirement: required limit, coverage type, certificate language, any additional-insured wording, and the deadline. Then separately confirm whether the prime is also requesting CMMC status, an SPRS score, NIST 800-171 evidence, or CUI-scope information.

Is GCC High required for cyber insurance?

Not universally. GCC High, AWS GovCloud, and CUI enclaves are scope-and-contract questions. Underwriters may ask about cloud security, but your CMMC and CUI obligations come from your contract and from where FCI/CUI is processed, stored, or transmitted.

What should I never upload into a matching or insurance form?

Never submit CUI, drawings, technical data, export-controlled files, source code, contract deliverables, incident details, credentials, or sensitive contract documents. Use high-level scope, level, environment, and timeline only.

The bottom line

Cyber insurance for defense contractors works best when you stop treating it as a checkbox and start treating it as one coordinated step inside your larger CMMC path. Buy the coverage you actually need — from a licensed broker who understands DoD flow-downs — after you’ve built and documented the security posture that both underwriters and the Department of Defense expect. The two reinforce each other. The same evidence that earns a defensible insurance application earns a defensible affirmation, and the same false statement that voids a policy can put you in front of the Department of Justice.

Need help deciding what type of CMMC provider you need?

Tell us your level, scope, and timeline, and we’ll match you with source-checked CMMC provider options.

Find My CMMC Path →If you’re earlier in the journey and just want to get organized, our CMMC Readiness Checklist mapped to the 14 NIST 800-171 families is a self-serve next step. Choose the right CMMC path before you hire.

Disclosure

How we researched this (methodology)

- DFARS 252.204-7012 clause text — the 72-hour reporting definition, 90-day preservation, DC3 malware submission, FedRAMP Moderate equivalency for cloud handling covered defense information, and DoD’s May 2024 class deviation keeping NIST SP 800-171 Revision 2 as the operative standard.

- The CMMC timeline: 32 CFR Part 170 effective December 16, 2024; DFARS 252.204-7021 and 252.204-7025, effective November 10, 2025; Phase 1 through November 9, 2026; Phase 2 beginning November 10, 2026.

- NIST SP 800-171 Rev. 2 as the controlling baseline for CMMC Level 2 — 110 requirements across 14 families.

- DOJ Civil Cyber-Fraud Initiative settlement record, including Georgia Tech and MORSE DOJ announcements read directly.

- Lloyd’s Market Bulletin Y5381 (state-backed cyber-attack exclusions, effective March 31, 2023) and the Merck v. ACE American NotPetya litigation and January 2024 settlement.

- The Cyber AB CMMC Code of Professional Conduct (v2.0) three-year consulting/assessment separation rule.

- Cyber insurance market data from the NAIC 2025 report (U.S. direct written premium ~$9.14B in 2024, first-ever decline; claims up nearly 40%) and Marsh’s market updates.

Related reading

- Does Cyber Insurance Require CMMC? — primary-sourced answer with the 3-document test and NIST crosswalk

- Find My CMMC Path — map your level, scope, and timeline to the right provider category

- CMMC Readiness Checklist — 14 NIST 800-171 families, self-serve

- CMMC Levels Explained

- CMMC Cost

- CMMC Provider Categories

- SPRS Score

- CMMC Secure Enclave

- GCC High Cost and Licensing

- AWS GovCloud for CMMC

- Azure Government for CMMC

- Best CMMC Consultants for Defense Contractors

- CMMC RPO Consultants